Short Sales Are Making a Comeback in Aubrey and Little Elm: What Homeowners Need to Know

Short Sales Are Making a Comeback in Aubrey and Little Elm: What Homeowners Need to Know

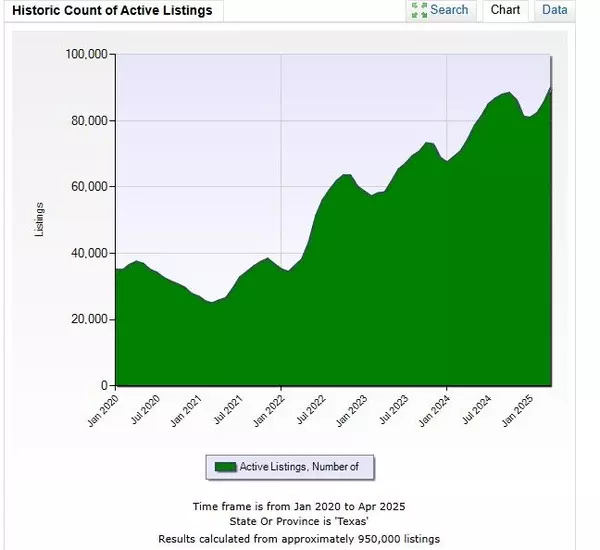

Over the past several months, we have started seeing a noticeable increase in short sale and cash-for-keys conversations throughout Aubrey, Little Elm, Cross Roads, Oak Point, Providence Village, Savannah, and the US-380 Corridor. More homeowners are realizing they may owe too much on their mortgage compared to what their home is currently worth. In many cases, the home is not selling fast enough, price reductions are stacking up, and the numbers simply do not work after factoring in payoff amounts, closing costs, commissions, taxes, insurance, and repairs.

This does not mean every homeowner is in trouble. However, it does mean some sellers need to understand their options before the situation gets worse.

What Is a Short Sale?

A short sale happens when a lender agrees to let a homeowner sell the property for less than the total amount owed on the mortgage.

For example, if a homeowner owes $425,000 but the home may only sell for $395,000, there may not be enough money from the sale to pay off the loan, closing costs, and selling expenses. In that situation, the lender may review the file and decide whether accepting a short sale is better than pursuing foreclosure.

Why Are More Homeowners Facing This?

Several factors are creating pressure in parts of the Aubrey and Little Elm housing market.

- Higher mortgage payments: Many homeowners bought when prices were high and interest rates were rising.

- Higher taxes and insurance: Monthly housing costs have increased for many families across North Texas.

- More inventory: More listings mean buyers have more choices, which can lead to longer days on market and price reductions.

- Life changes: Divorce, job loss, relocation, medical issues, and income changes can quickly create financial stress.

- Too little equity: Some sellers simply do not have enough equity to cover the full payoff and cost of selling.

The Short Sale Process

1. Determine the Current Market Value

The first step is getting a realistic market analysis. The home must be priced based on current buyer demand, comparable sales, active competition, and neighborhood trends.

2. Review the Mortgage Payoff

The seller needs to know the exact mortgage payoff amount, including any missed payments, late fees, escrow shortages, or additional liens.

3. Contact the Mortgage Servicer

The lender or mortgage servicer must be contacted to begin the short sale review process. Most lenders require a hardship package before they will consider approving a short sale.

4. Gather Financial Documents

Common short sale documents may include:

- Hardship letter

- Mortgage statement

- Bank statements

- Pay stubs

- Tax returns

- Monthly expense worksheet

- Listing agreement

- Purchase contract once an offer is received

5. List and Market the Home

The home is listed for sale and marketed to buyers. The goal is to generate the strongest possible offer that the lender may be willing to approve.

6. Submit the Offer to the Lender

Once an offer is received, the short sale package is submitted to the lender. The lender reviews the offer, the seller’s financial hardship, the market value, and the estimated net proceeds.

7. Wait for Lender Approval

Short sales are not always fast. Approval can take weeks or even months depending on the lender, the loan type, and whether there are multiple liens.

8. Close the Sale

If the lender approves the short sale, the transaction moves toward closing. The seller transfers ownership, and the lender accepts the approved payoff amount.

What Is Cash for Keys?

Cash for keys is different from a short sale. It usually happens when a lender, bank, investor, or new owner offers money to an occupant in exchange for leaving the home by an agreed date and keeping the property in acceptable condition.

For homeowners who are already behind or facing foreclosure, cash for keys may help cover moving expenses and avoid a more stressful eviction process.

Is a Short Sale Better Than Foreclosure?

A short sale may give the homeowner more control than foreclosure. It may also allow the seller to avoid some of the uncertainty, stress, and public consequences of a foreclosure process.

Every situation is different, so homeowners should speak with their lender, a qualified real estate professional, and, when needed, a real estate attorney or tax advisor before making a decision.

What Should You Do If You Owe More Than Your Home Is Worth?

The worst move is ignoring the problem. If you are behind on payments, worried about foreclosure, or concerned your home may not sell for enough to pay everything off, it is better to review your options early.

You may still have several possible paths, including a traditional sale, price adjustment, short sale, loan modification, repayment plan, deed-in-lieu, or cash-for-keys solution.

At Justin Henry Real Estate Advisors, we help homeowners throughout Aubrey, Little Elm, Cross Roads, Oak Point, Providence Village, Savannah, and the 380 Corridor understand their home value, review selling options, and make informed decisions before foreclosure becomes the only option.

Categories

- All Blogs (33)

- 5 things before winter (1)

- aubrey (4)

- aubrey homes (5)

- Builder (1)

- buy (3)

- buying (6)

- Dallas (10)

- discount homes (1)

- equity (4)

- home buying (2)

- Home Sales (10)

- homes (8)

- homes in aubrey (2)

- homes with pools (2)

- inventory (1)

- leasing (2)

- little elm homes (3)

- multiple offers (2)

- Painting The Room, Should you paint, painting before selling, selling your home in little elm, get your home painted (1)

- pool house (2)

- price (7)

- real estate negotiations, (2)

- Staging (4)

- taxes (3)

- Window Coverings, energy efficeint windows (1)

- winter (2)

- winter in texas (2)

Recent Posts

26875 US Hwy 380 # 112, Aubrey, TX, 76227, United States